RESERVE BANK OF INDIA

RBI was established on April 1, 1935 in accordance with the provisions of the Reserve Bank of India Act/1934.

The Central bank was formed under the recommendations from John Hilton Young Commission 1926, also called Royal Commission of Indian Currency and Finance.

The Central Office of the Reserve Bank was initially established in Calcutta but was permanently moved to Mumbai in 1937.

Though originally privately owned, since nationalization in 1949, the Reserve Bank is fully owned by the Government of India.

CONSTITUTION

The Reserve Bank's affairs are governed by a central board of directors. The board is appointed by the Government of India in keeping with the Reserve Bank of India Act.

Appointed/nominated for a period of four years.

Present Governor

Dr. Urjit R. Patel (24th Governor)

Deputy Governors

Shri BP Kanungo

Shri S. S. Mundra

Shri N. S. Vishwanathan

Dr. Viral V. Acharya

First Governor of RBI - Sir Osbome Smith First Indian Governor of RBI - C. D. Deshmukh

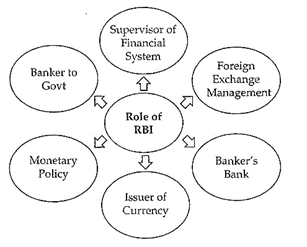

Functions of Reserve Bank of India

Monetary Authority:

Formulates, implements and monitors the monetary policy.

Objective: maintaining price stability and ensuring adequate flow of credit to productive sectors.

Regulator and supervisor of the financial system:

Prescribes broad parameters of banking operations within which the country's banking and financial system functions. Objective: maintain public confidence in the system, protect depositors' interest and provide cost-effective banking services to the public.

Manager of Foreign Exchange:

Manages the Foreign Exchange Management Act, 1999.

Objective: to facilitate external trade and payment and promote orderly development and maintenance of foreign exchange market in India.

Issuer of currency:

Issues and exchanges or destroys currency and coins not fit for circulation.

Objective: to give the public adequate quantity of supplies of currency notes and coins and in good quality.

Developmental role:

Performs a wide range of promotional functions to support national objectives.

Banker to the Government:

Performs merchant banking functions for the central and the state governments; also acts as their banker.

Banker to banks:

Maintains banking accounts of all scheduled banks.

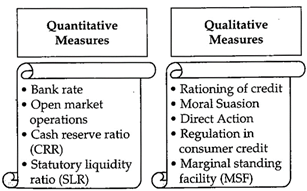

INSTRUMENTS OF MONETARY POLICY - QUANTITATIVE & QUALITATIVE TOOLS

The instruments of monetary policy are tools or devices which are used by the monetary authority in order to attain some predetermined objectives.

ELEMENTS OF MONETARY POLICY

REPO AND REVERSE REPO RATE

Repo is a transaction wherein securities are sold by the RBI and simultaneously repurchased at a fixed price. This fixed price is determined in context of an interest rate called the repo rate. The higher the repo rate, more costly are the funds for banks and hence, higher will be more...

MONEY AND ITS TYPES

Money: Money is anything that is widely accepted in exchange for goods and services.

Types of Money

Commodity Money - Commodity money is the type of Money that is in the form of a commodity with intrinsic value which means it has value outside of its use as money. The commodity itself represents money, and the money is the commodity. Example: Gold silver, copper, salt, peppercorns, rice, large stones, etc.

Representative Money - It actually represents Money. It is exchangeable for a commodity. Examples: Token coins, or any other physical tokens like certificates.

Fiat Money - It is whose value is not derived from any intrinsic value or any guarantee that it can be converted into valuable commodity (like gold). It has value as money because a government decreed that it has value for that purpose.

Money Market

Money Market is a short-term credit market. The Money Market is regulated by the Reserve Bank of India. It is the centre in which short- term funds are borrowed and lent. It consists of borrowers and lenders of short-term funds.

The lenders are commercial banks, insurance companies, finance companies and the central bank. The money market brings together the lenders and the borrowers.

RBI approach of money supply

The RBI controls the money supply in the economy by various means.

Various measures of money supply are: Reserve Money (MO): Notes and coins + reserves of banks with central bank

currency with the public demand deposits+ other deposits held with the RBI.

savings deposits with post office savings banks

time deposits

total deposits with the post office savings organization.

MONEY MARKET INSTRUMENTS

Treasury Bills

Commercial Papers

Certificate of Deposit

Banker's Acceptance

Repurchase Agreement

Treasury Bills:

Treasury bills (T-bills) offer short-term investment opportunities, generally up to one year. They are thus useful in managing short- term liquidity. At present, the Government of India issues three types of treasury bills through auctions, namely, 91-day, 182-day and 364-day. There are no treasury bills issued by State Governments.

Minimum Price:

Treasury bills are available for a minimum amount of Rs. 25,000 and in multiples of Rs. 25,000. Treasury bills are issued at a discount and are redeemed at par. Treasury bills are also issued under the Market Stabilization Scheme (MSS).

Commercial Paper and Certificates of Deposits

Certificate of Deposit

Commercial Paper (CP)

Certificate of Deposit (CD) is a negotiable money market instrument and issued in demat form or as a Usance Promissory Note against funds deposited at a bank or other eligible financial institution for a specified time period.

Commercial Paper (CP) is an unsecured money market instrument issued in the form of a promissory note. It was introduced in India in 1990 with a view to enabling highly rated corporate borrowers.

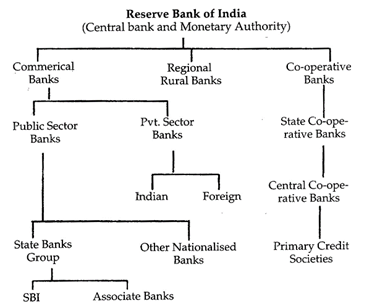

INDIAN BANKING SYSTEM

COMMERCIAL BANKS

Commercial bank is an institution that accepts deposits, makes business loans and offers related services to general public and businessmen. Commercial banks in India are largely Indian public sector and private sector with a few foreign banks. The public sector banks account for more than 80 percent of the entire banking business in India occupying a dominant position in the commercial banking. These are a profit making institution owned by government or private or both.

There are currently 27 public sector banks in India out of which 19 are nationalised banks and 6 are SBI and its associate banks, and rest two are IDBI Bank and Bharatiya Manila Bank, which are categorised as other public sector banks. There are total 93 commercial banks in India.

Public sector banks:

There are currently 27 public sector banks in India out of which 20 are nationalized banks and 6 are SBI and its associate banks, and last is Bharatiya Mahila Bank, which is categorised as other public sector bank. There are total 93 commercial banks in India.

The public sector accounts for 80 percent of total banking business in India and State Bank of India is the largest commercial bank in terms of volume of all commercial banks. b. Private sector banks:

Private sector banks are those whose

Private sector banks are those whose equity is held by private shareholders. For example, ICICI, HDFC etc. Private sector banks play a major role in the development of Indian banking industry.

Differences between Private and Public Sector Banks

Private sector banks introduced the concept of online banking in India. This was mostly because the private banks were technologically well equipped.

· Private sector banks were using state-of-the-art technology and fully computerized systems since the time they entered the Indian market whereas the Public sector banks were not.

· Despite the technological challenges, the public sector banks are still the preferred destinations for many as they are considered as safer options for money deposit.

Foreign Banks:

Foreign banks are those banks which have their head offices abroad. These banks have their registered head offices in a foreign country, while they operate their branches in India. They can operate in India either through wholly-owned subsidiaries or through branches. CITI bank, HSBC, Standard Chartered etc. are the examples of foreign banks in India.

REGIONAL RURAL BANK (RRB)

These are state sponsored regional rural oriented banks. They provide credit for agricultural and rural development. The main objective of RRB is to develop rural economy. Their borrowers include small and marginal farmers, agricultural labourers, artisans etc. NABARD holds the apex position in the agricultural and rural development.

After nationalization of banks in 1960, there were problems which made it difficult for more...

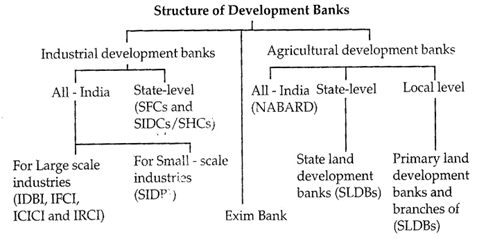

Development banks are specialized financial institutions.

They provide medium and long-term finance to the industrial and agricultural sectors

They provide finance to both private and public sectors.

They do term lending, investment in securities and other activities.

They even promote saving and investment habits in the public.

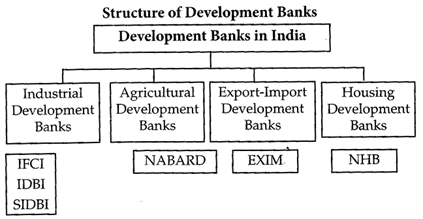

Development banks in India are classified into following four groups;

Industrial Development Banks

They include for example. Industrial Finance Corporation of India (IFCI), Industrial Development Bank of India (IDBI), and Small Industries Development Bank of India (SIDBI).

Industrial Finance Corporation of India (IFCI)

The IFCI was the first specialised financial institution set up in India to provide term finance to large industries in India. It was established on 1st July, 1948 under the Industrial Finance Corporation Act of 1948.

Objectives of IFCI

The main objective of IFCI is to provide medium and long term financial assistance to large scale industrial undertakings, particularly when ordinary bank accommodation does not suit the undertaking or finance cannot be profitably raised by it from the issue of shares.

Functions of IFCI:

For setting up a new industrial undertaking.

For expansion and diversification of existing industrial undertaking.

For renovation and modernisation of existing concerns.

For meeting the working capital requirements of industrial concerns in some exceptional cases.

Industrial Development Bank of India (IDBI)

Industrial development Bank of India (IDBI) came into being on 1st July, as a Development Institutions under IDBI Act 1964. It is headquartered at Mumbai.

It is regarded as a Public Financial Institution in terms of Companies Act. It continued as DPI till 2004 when it was transferred into a Bank. To transform this into Bank/ Industrial Development Bank Act 2003 was passed.

A new company under the name of Industrial Development Bank of India Ltd. was incorporated as a Govt company under the Companies Act on 27th September, 2004, and thus now it came to be known as IDBI Ltd w.e.f 1st October 2004 but it also worked as a Bank in terms of the Repeal Act.

With effect from 2nd April, 2005, IDBI Bank Ltd was finally amalgamated with IDBI Ltd and was known as IDBI Ltd. It is a Public Sector Bank as government has above 70% shareholding in this Bank.

SIDBI

Small Industries Development Bank of India (SIDBI) was set up under an Act of Parliament in 1990. Though it was a wholly owned subsidiary of Industrial Development Bank of India, presently the ownership is held by 33 Government of India owned / controlled institutions. It is headquartered in Lucknow.

Functions:

Credit Functions of Banks

The two most distinctive features of a commercial bank are borrowing and lending, i.e. acceptance of deposits and lending of money to projects to earn Interest (profit). In short, banks borrow to lend. The rate of interest offered by the banks to depositors is called the borrowing rate while the rate at which banks lend out is called lending rate.

The difference between the rates is called 'spread' which is appropriated by the banks. All financial institutions are not commercial banks but only those which perform dual functions of

(i) accepting deposits and

(ii) giving loans - are termed as commercial banks. For example post offices are not bank because they do not give loans. Functions of commercial banks are classified into two main categories - (A) Primary functions and (B) Secondary functions.

(A) PRIMARY FUNCTIONS:

Accepting deposits:

A commercial bank accepts deposits in the form of current, savings and fixed deposits. It collects the surplus balances of the Individuals, firms and finances the temporary needs of commercial transactions. The first task is, therefore, the collection of the savings of the public. The bank does this by accepting deposits from its customers. Deposits are the lifeline of banks.

DEPOSITS ARE OF THREE TYPES AS UNDER:

(i) Current account deposits:

Such deposits are payable on demand and are, therefore, called demand deposits. These can be withdrawn by the depositors any number of times depending upon the balance in the account. The bank does not pay any Interest on these deposits but provides cheque facilities. These accounts are generally maintained by businessmen and Industrialists who receive and make business payments of large amounts through cheques.

(ii) Fixed deposits (Time deposits):

Fixed deposits have a fixed period of maturity and are referred to as time deposits. These are deposits for a fixed term, i.e., period of time ranging from a few days to a few years. These are neither payable on demand nor they enjoy cheque facilities.

They can be withdrawn only after the maturity of the specified fixed period. They carry higher rate of interest. They are not treated as a part of money supply Recurring deposit in which a regular deposit of an agreed sum is made is also a variant of fixed deposits.

(iii) Savings account deposits:

These are deposits whose main objective is to save. Savings account is most suitable for individual households. They combine the features of both current account and fixed deposits. They are payable on demand and also withdrawable by cheque. But bank gives this facility with some restrictions, e.g., a bank may allow four or five cheques in a month. Interest paid on savings account deposits is lesser than that of fixed deposit.

Difference between demand deposits and time (term) deposits: Two traditional forms of deposits are demand deposit and term (or time) deposit:

(i) Deposits which can be withdrawn on demand by depositors are called demand deposits, e.g. current account deposits are called more...

Challenges in Banking System

Our banking system, at present juncture, is facing significant challenges from several quarters. These challenges, if not addressed quickly and adequately, may result in loss of opportunities as and when the economic growth starts picking up momentum.

In a sense, it has implications for both- the banks as well as the economy as a whole, because a strong banking system is one of the essential pre-requisites in the quest for growth.

NON-PERFORMING ASSETS (NPAs)

A non-performing asset (NPA) is a loan or advance for which the principal or interest payment remained overdue for a period of 90 days.

Description: Banks are required to classify NPAs further into Substandard, Doubtful and Loss assets.

Substandard assets: An Asset which has remained NPA for a period of less than or equal to 12 months.

Doubtful assets: An asset would be classified as doubtful if it has remained in the substandard category for a period of 12 months.

Loss assets: As per RBI, "Loss asset is considered uncollectible and of such little value that its continuance as a bankable asset is not warranted, although there may be some salvage or recovery value."

Bad loans now constitute 11 per cent of the gross advances of PSU banks, while total NPAs, including those for public and private banks, were Rs. 697,409 crore as of December 2016.

Presidential Ordinance on NPA

The Presidential Ordinance empowered the Reserve Bank of India to enforce expeditious resolution of non-performing assets of banks.

This initiative will boost legal empowerment of the central bank to crack down on NPAs of banks.

The ordinance will have impact on the economy, the banking sector's lending behaviour and the country's investment climate.

Union government has now empowered itself to direct the RBI to take necessary steps to initiate the NPA resolution process once a default has been established.

It projects the role of the political establishment as a proactive agent in bank NPA resolution.

It can also lead to a political risk because this will expose the government and the political establishment to charges of having used discretion to pick and choose the default cases requiring NPA resolution.

The provisions of the Bankruptcy Code have now been linked to the Banking Regulation Act.

It also allows the RBI to set up oversight committees for banks with NPAs.

Stressed Assets

Stressed accounts are the ones that show incipient signs of becoming NPA – like bounced cheques/ not submitting financial data/ stock shortages/ request for frequent overdrawal of account etc.

Stressed assets = NPAs + Restructured loans + Written off assets

Restructured assets or loans are those assets which got an extended repayment period, reduced interest rate, converting a part of the loan into equity, providing additional financing/ or some combination of these measures. Hence, under restructuring a bad loan is modified as a new loan. But the real problem is that it was actually an NPA.

Hence, the restructured loan is also more...

Financial Inclusion

"Financial inclusion is delivery of banking services at an affordable cost ('no frills' accounts,) to the vast sections of disadvantaged and low income group. As banking services are in the nature of public good, it is essential that availability of banking and payment services to the entire population without discrimination is the prime objective of the public policy."

Importance of FINANCIAL INCLUSION

The policy makers have been focusing on Financial Inclusion of Indian rural and semirural areas primarily for three most important pressing needs.

Creating a platform for inculcating the habit to save MONEY – The lower income category has been living under the constant shadow of financial duress mainly because of the absence of savings. The absence of savings makes them a vulnerable lot. Presence of banking services and products aims to provide a critical tool to inculcate the habit to save. Capital formation in the country is also expected to be boosted once financial inclusion measures materialize, as people move away from traditional modes of parking their savings in land, buildings, bullion, etc.

Providing formal credit avenues – So far the unbanked population has been vulnerably dependent of informal channels of credit like family, friends and moneylenders. Availability of adequate and transparent credit from formal banking channels shall allow the entrepreneurial spirit of the masses to increase outputs and prosperity in the countryside,

Plug gaps and leaks in public subsidies and welfare programmes – A considerable sum of money that is meant for the poorest of poor does not actually reach them. While this money meanders through large system of government bureaucracy, much of it is widely believed to leak and is unable to reach the intended parties. Government is therefore, pushing for direct cash transfers to beneficiaries through their Bank Accounts rather than subsidizing products and making cash payments.

Steps taken to support FINANCIAL INCLUSION

Banking services reach homes through business correspondents - The banking systems have started to adopt the business correspondent mechanism to facilitate banking services in those areas where banks are unable to open brick and mortar branches for cost considerations. Business Correspondents provide affordability and easy accessibility to this unbanked population. Armed with suitable technology, the business correspondents help in taking the banks to the doorsteps of rural households. So far, 110,000 business correspondents have been employed through the business facilitator and business correspondent

(BC) models and set up goals for banks to provide access to formal banking to all 74,414 villages with population over 2000.

No-frills accounts: These accounts provide basic facilities of deposit and withdrawal to accountholders makes banking affordable by cutting down on extra frills that are no use for the lower section of the society. These accounts are expected to provide a low-cost mode to access Bank Accounts. RBI also eased KYC (Know Your customer) norms for opening of such accounts.

Kisan Credit Card (KCC) - from the year 1998-99, to meet production credit requirements more...

Modern Aspects of Banking

Technology has transformed the global world of banking and financial services beyond recognition. No other industry offers more complex challenges and more exciting opportunities than banking. Computerization of the business of banks has been receiving great importance. The banking institutions have already crossed 70% level of computerization of their businesses.

AUTOMATED TELLER MACHINE

Automated Teller Machine is a computerized machine that provides the customers of banks the facility of accessing their account for dispensing cash and to carry out other financial and non-financial transactions without the need to actually visit their bank branch.

Types of ATMs

Onsite ATMs: This type of ATM is situated either within the branch premises or in very close proximity of the branch.

Offsite ATMs: It is not situated within the branch premises but is located at other places, such as malls, petrol stations etc

Worksite ATMs: It is located within the premises of an organisation and is generally meant only for the employees of the organisation.

White Label ATMs (WLA): ATM is set up, owned and operated by non-banks is called White Label ATM. Non-ATM operators are authorized under Payment & Settlement Systems Act, 2007 by the RBI. However in White ATMs acceptance of cash deposits is not permitted.

Brown Label ATMs: 'Brown label' ATMs are those whose hardware and the lease of the ATM machine is owned by a service provider, but cash management and connectivity to banking networks is provided by a sponsor bank Whose brand used the ATM.

Free transactions at ATMs: With effect from November 01, 2014, a bank must offer to its savings bank account holders a minimum number of free transactions at ATMs. However, it is not applicable to Basic Savings Bank Deposit Accounts (BSBDA) as withdrawals from BSBDA are subject to the conditions associated with such accounts.

Transactions at any other bank's ATMs at Metro locations: In case of ATMs located in six metro locations, viz Mumbai, New Delhi/ Chennai, Kolkata, Bengaluru and Hyderabad, banks must Offer their savings account holders a three-time free transactions (Including financial and transactions) in a month.

Failed ATM transaction:

The customer should file a complaint with the card issuing bank at the earliest. This is applicable even if it was carried out at another bank's/non-bank's ATM.

Banks have been mandated to resolve Customer complaints by re-crediting the customer's account within 7 working days from the date of complaint. However, if the complaint raised by the customer is not resolved, banks have to pay Rs. 100 a day for delays in re-crediting the amount within 7 working days from the date of receipt of complaint.

The compensation has to be credited to the account of the customer without any Claim being made by the customer. If the complaint is not lodged within 30 days of transaction, the customer is not entitled for any compensation for delay in resolving his/ her complaint.

Credit Card

A credit card is a Plastic card issued more...

BHARAT BILL PAYMENT SYSTEM (BBPS)

Bharat Bill Payment System (BBPS) is an integrated bill payment system which will offer interoperable bill payment service to customers online as well as through a network of agents on the ground. The system will provide multiple payment modes and instant confirmation of payment.

With a need of bill payments system, various organizations decided to provide a single platform to make all these payments. So an integrated bill payment system called BBPS was proposed for which the policy guidelines were issued by the Reserve Bank of India on November 28, 2014.

National Payment Corporation (NPCI) is identified to act as Bharat Bill Payment Central Unit (BBPCU) which will be a single authorized entity for operating the BBPS.

The biggest advantage is that the bill can be paid anywhere and anytime. The system will provide multiple payment modes and instant confirmation of payment. Payments may be made through the BBPS using cash, transfer cheques, and electronic modes. The BBPS outlets would include banks, ATMs, business correspondents, kiosks etc.

Aadhaar Enabled Payment System

AEPS is to further speed track Financial Inclusion in the country; it is a bank led model which allows online interoperable financial inclusion transaction at POS (Micro ATM) through the Business correspondent of any bank using the Aadhaar authentication. The Aadhaar enabled basic types of banking transactions are as follows:-

Balance Enquiry

Cash Withdrawal

Cash Deposit

Aadhaar to Aadhaar Funds Transfer

The only inputs required for a customer to do a transaction under this scenario are:-

IIN (Identifying the Bank to which the customer is associated)

Aadhaar Number

Fingerprint captured during their enrolment

Unified Payment Interface

Unified Payment Interface was officially launched by National Payments Corporation of India (NPCI), under RBI for instant inter-bank real time transactions using android apps.

UPI is a payment system that allows money transfer between any two bank accounts by using a smartphone.

UPI allows a customer to pay directly from a bank account to different merchants, both online and offline, without the hassle of typing credit card details, IFSC code, or net banking/wallet passwords.

Para Banking Services

Para banking activities refer to those activities carried out by the bank which are other than their normal day-to-day activities (deposits withdrawals, giving credit/ etc.). The Para Banking activities include insurance business, portfolio management services, pension fund management, mutual funds business, money market mutual funds underwriting of bonds of PSUs, investment in venture capital funds, etc. The para Banking activities which can be performed by bank have been permitted by KBI. Banks can do these activities either departmentally or by setting up subsidiaries to undertake the type of business.

SUBSIDIARIES OF BANKS

Banks are allowed to form subsidiaries as per Section 19(1) of the Banking Regulation Act, 1949. Banks can invest up to 10 percent of their capital in the subsidiaries.

Banks may form a subsidiary company tor undertaking the types of businesses which a banking company is otherwise permitted to undertake, with prior approval of Reserve Bank of India

Most well-known banks today have subsidiaries, which offer numerous financial services, such as dealing with mutual funds leasing equipment, or investing in venture capital funds (VCF).

Some well-known subsidiaries of major banks m India that offer para-banking services include SBI Pension Funds Private Ltd, SBI Mutual Fund, ICICI Ventures, ICICI Prudentials, HDFC Securities (HS), and more. Not only individuals, but companies too, avail these services. These financial services help people or companies to manage their assets, invest funds profitably, etc.

Activities of Indian Banks which come under Para Banking are as follows -

Banks' investment in Venture Capital Funds (VCFs)

Banks as sponsors to Infrastructure Debt Funds

Equipment leasing. Hire purchase business and Factoring services

Primary Dealership business

Underwriting of Corporate Shares and Debentures

Underwriting of bonds of Public Sector Undertakings

Retailing of Government Securities

Mutual Fund Business

Money Market Mutual Funds (MMMFs)

Cheque biting Facility for Investors of MMMFs

Insurance business

Pension Fund Management (PFM) by banks

Referral Services

Membership of SEBI approved Stock exchanges

Portfolio Management Services

Safety Net' Schemes

Disclosure of commissions/ remunerations

Relationship with Subsidiaries

A sponsor bank is required to maintain an arm’s length" relationship with the subsidiary/ mutual fund sponsored by it in regard to business parameters such as, taking undue advantage in borrowing/lending funds, transferring/selling/ buying of securities at rates other than market rates, giving special consideration for securities transactions, overindulgence in supporting/ financing the subsidiary, financing the bank's clients through them when the bank itself is not able or is not permitted to do so, etc. Supervision by the parent bank should not, however, result in interference in the day-to-day management of the affairs of the subsidiary/mutual fund.

Relationship with Systemically Important Non-Banking Financial Companies

The regulatory gaps in the area of bank and NBFC operations contribute to creating the possibility of regulatory arbitrage and hence may give rise to an uneven playing field and systemic risk. As such banks are advised to follow the regulatory framework mentioned below as regards their relationship with systemically important NBFCs:

(a) more...

Monetary Authority:

Formulates, implements and monitors the monetary policy.

Objective: maintaining price stability and ensuring adequate flow of credit to productive sectors.

Regulator and supervisor of the financial system:

Prescribes broad parameters of banking operations within which the country's banking and financial system functions. Objective: maintain public confidence in the system, protect depositors' interest and provide cost-effective banking services to the public.

Manager of Foreign Exchange:

Manages the Foreign Exchange Management Act, 1999.

Objective: to facilitate external trade and payment and promote orderly development and maintenance of foreign exchange market in India.

Issuer of currency:

Issues and exchanges or destroys currency and coins not fit for circulation.

Objective: to give the public adequate quantity of supplies of currency notes and coins and in good quality.

Developmental role:

Performs a wide range of promotional functions to support national objectives.

Banker to the Government:

Performs merchant banking functions for the central and the state governments; also acts as their banker.

Banker to banks:

Maintains banking accounts of all scheduled banks.

INSTRUMENTS OF MONETARY POLICY - QUANTITATIVE & QUALITATIVE TOOLS

The instruments of monetary policy are tools or devices which are used by the monetary authority in order to attain some predetermined objectives.

ELEMENTS OF MONETARY POLICY

Monetary Authority:

Formulates, implements and monitors the monetary policy.

Objective: maintaining price stability and ensuring adequate flow of credit to productive sectors.

Regulator and supervisor of the financial system:

Prescribes broad parameters of banking operations within which the country's banking and financial system functions. Objective: maintain public confidence in the system, protect depositors' interest and provide cost-effective banking services to the public.

Manager of Foreign Exchange:

Manages the Foreign Exchange Management Act, 1999.

Objective: to facilitate external trade and payment and promote orderly development and maintenance of foreign exchange market in India.

Issuer of currency:

Issues and exchanges or destroys currency and coins not fit for circulation.

Objective: to give the public adequate quantity of supplies of currency notes and coins and in good quality.

Developmental role:

Performs a wide range of promotional functions to support national objectives.

Banker to the Government:

Performs merchant banking functions for the central and the state governments; also acts as their banker.

Banker to banks:

Maintains banking accounts of all scheduled banks.

INSTRUMENTS OF MONETARY POLICY - QUANTITATIVE & QUALITATIVE TOOLS

The instruments of monetary policy are tools or devices which are used by the monetary authority in order to attain some predetermined objectives.

ELEMENTS OF MONETARY POLICY

REPO AND REVERSE REPO RATE

Repo is a transaction wherein securities are sold by the RBI and simultaneously repurchased at a fixed price. This fixed price is determined in context of an interest rate called the repo rate. The higher the repo rate, more costly are the funds for banks and hence, higher will be more...

REPO AND REVERSE REPO RATE

Repo is a transaction wherein securities are sold by the RBI and simultaneously repurchased at a fixed price. This fixed price is determined in context of an interest rate called the repo rate. The higher the repo rate, more costly are the funds for banks and hence, higher will be more...  COMMERCIAL BANKS

Commercial bank is an institution that accepts deposits, makes business loans and offers related services to general public and businessmen. Commercial banks in India are largely Indian public sector and private sector with a few foreign banks. The public sector banks account for more than 80 percent of the entire banking business in India occupying a dominant position in the commercial banking. These are a profit making institution owned by government or private or both.

There are currently 27 public sector banks in India out of which 19 are nationalised banks and 6 are SBI and its associate banks, and rest two are IDBI Bank and Bharatiya Manila Bank, which are categorised as other public sector banks. There are total 93 commercial banks in India.

COMMERCIAL BANKS

Commercial bank is an institution that accepts deposits, makes business loans and offers related services to general public and businessmen. Commercial banks in India are largely Indian public sector and private sector with a few foreign banks. The public sector banks account for more than 80 percent of the entire banking business in India occupying a dominant position in the commercial banking. These are a profit making institution owned by government or private or both.

There are currently 27 public sector banks in India out of which 19 are nationalised banks and 6 are SBI and its associate banks, and rest two are IDBI Bank and Bharatiya Manila Bank, which are categorised as other public sector banks. There are total 93 commercial banks in India.

Development banks in India are classified into following four groups;

Industrial Development Banks

They include for example. Industrial Finance Corporation of India (IFCI), Industrial Development Bank of India (IDBI), and Small Industries Development Bank of India (SIDBI).

Industrial Finance Corporation of India (IFCI)

The IFCI was the first specialised financial institution set up in India to provide term finance to large industries in India. It was established on 1st July, 1948 under the Industrial Finance Corporation Act of 1948.

Objectives of IFCI

The main objective of IFCI is to provide medium and long term financial assistance to large scale industrial undertakings, particularly when ordinary bank accommodation does not suit the undertaking or finance cannot be profitably raised by it from the issue of shares.

Functions of IFCI:

Development banks in India are classified into following four groups;

Industrial Development Banks

They include for example. Industrial Finance Corporation of India (IFCI), Industrial Development Bank of India (IDBI), and Small Industries Development Bank of India (SIDBI).

Industrial Finance Corporation of India (IFCI)

The IFCI was the first specialised financial institution set up in India to provide term finance to large industries in India. It was established on 1st July, 1948 under the Industrial Finance Corporation Act of 1948.

Objectives of IFCI

The main objective of IFCI is to provide medium and long term financial assistance to large scale industrial undertakings, particularly when ordinary bank accommodation does not suit the undertaking or finance cannot be profitably raised by it from the issue of shares.

Functions of IFCI: