Financial Marketing

Category :

10. Financial Markets

INTRODUCTION

The chapter brings into focus the concept and types of financial markets, money market, its instruments, and primary and secondary types of Capital market. It describes the meaning and function of stock exchange, the objectives and functions of SEBI.

Chapter at a Glance

CONCEPT OF FINANCIAL MARKET

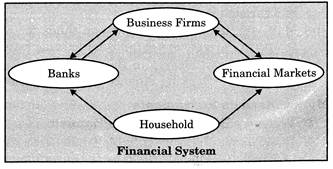

In every economy, there are two main sectors:

1. Households: They save funds and are known as 'Savers'.

2. Business Firms: They invest funds and are known as 'investors'.

Financial market acts as a link or an intermediary between these two sectors. It enables the savers to invest their surplus funds and enable the investors to borrow funds to meet their requirements. In doing so, it performs 'Allocative Functions'.

Allocative function of financial market refers to linking the savers and investors by mobilizing funds between them. While performing the allocative function, two consequences follow:

· The rate of return offered to household would be higher.

· Scarce resources are allocated to those firms which have the highest productivity for the economy.

There are two mechanisms, through which funds can be allocated or mobilized from households to business firms:

1. Banks: Households can deposit their surplus funds with banks, who in turn land these funds to business firms.

2. Financial Markets: Households can buy securities from the financial market to provide funds to business firms.

The process by which allocation of funds is done is called 'Financial Intermediation'. Both banks and financial markets provide various options to savers, to mobilize savings to investment opportunities. However, the scope of syllabus restricts the study to various aspects of Financial Market only.

Meaning of Financial Market

1. A financial market is a market for the creation and exchange of financial assets.

2. Financial markets exist wherever a financial transaction occurs.

3. Financial transactions could be either in the form of 'creation of financial assets' such as initial issue of securities by a firm or in the form of' exchange of financial assets' such as purchase and sale of existing securities.

Functions of Financial Market

1. Mobilisation of Savings And Channelizing Them Into The Most Productive Uses:

(i) A financial market facilitates the transfer of savings from savers to investors.

(ii) It gives savers the choice of different investments and thus helps to channelize surplus funds into the most productive use.

2. Facilitating Price Discovery:

(i) In the financial market, the households are suppliers of funds and business firms represent the demand.

(ii) Such forces of demand and supply help to establish a price for the financial asset which is being traded in that particular market.

3. Providing liquidity to Financial Assets:

(i) Financial markets provide liquidity to financial assets by facilitating easy purchase and sale of financial assets.

(ii) Holders of assets can readily sell their financial assets through the mechanism of the financial market.

4. Reducing the Cost of Transactions:

(i) The financial markets reduce the cost of transactions by providing a common platform where buyers and sellers can the purchase and sale of financial assets.

(ii) It helps to save time, effort and money that both buyers and sellers of a financial asset would have to otherwise spend of to try and find each other

Classification of Financial Markets

Financial markets are classified into two parts:

(a) Money Market (b) Capital Market

Let us explain in detail:

Money Market

(i) The money market is a market for short-term funds which deals in monetary assets whose period of maturity is up to one year.

(ii) In this market the risk is very less and highly liquid, unsecured and short term debts are traded. They are highly liquid because Discount Finance House of India (DFHI) provides a ready market for them.

(iii) It does not have any physical location, but it is an activity conducted over the telephone and through internet.

(iv) Main aim is to provide short run funds for meeting urgent requirement of cash and temporary investment of funds for earning returns.

(v) The major participants in the market are: Reserve Bank of India (RBI), Commercial Banks, and Non - Banking Finance companies, Mutual Funds, State govt. etc.

Money Markets Instruments

(i) Treasury Bill (Zero Coupon Bonds):

(a) Meaning: Treasury Bills (or T-bills) is an instrument (in the form of promissory note) of short-term borrowing by the government which is issued by the Reserve Bank of

India on behalf of the Government of India at discount for maturing in less than one year.

(b) Purpose: These are issued to meet short term requirements of funds.

(c) Period: These are issued for a period of 14 to 364 days.

(d) Amount: These are issued for a minimum amount of ` 25,000 and in multiple thereof.

(e) Issue Price: These are issued at a discount and are repaid at par. No interest is payable on these securities.

(f) Safety: These are considered as safe because of soundness of issuer i.e. RBI.

(g) Liquidity: These are highly liquid.

(h) Negotiability: These are negotiable instruments i.e. they are freely transferable by endorsement and delivery.

(i) Example: Suppose an investor purchases a 91 days Treasury bill with a face value of ` 1, 00,000 for ` 94,000. By holding the bill until the maturity date, the investor receives ` 1, 00,000. The difference of ` 6,000 between the proceeds received at maturity and the amount paid to purchase the bill represents the interest received by him.

(ii) Commercial Paper:

(a) Meaning: Commercial paper is a short-term unsecured promissory note, negotiable and transferable by endorsement and delivery with a fixed maturity period.

(b) Issuers: It is issued by financially sound reputed corporate enterprises.

(c) Period: These are issued for a period of 15 days to one year.

(d) Issue Price: These are sold at a discount and redeemed at par.

(e) Amount: They can be issued in denominations of ` 5 lakh and in multiple thereof.

(f) Purpose: It is used to raise short term funds at lower rates of interest than market rates.

(g) Negotiability: These are negotiable instruments i.e. they are freely transferable by endorsement and delivery.

(h) Investors: Usually the commercial banks and mutual funds invest in this instrument.

(i) Example: Suppose a Company needs long term finance to buy some Plant and Machinery. In order to raise the long term funds in the capital market the company will have to incur floatation costs (costs associated with floating of an issue such as brokerage, commission, printing of prospectus, application forms and advertising etc.) Commercial paper may be issued to meet the floatation costs. This is known as Bridge Financing.

(iii) Call Money:

(a) Meaning: Call money is short-term finance repayable on demand, with a maturity period of one day to fifteen days, used for inter- bank transactions.

(b) Purpose: The purpose of call money is to provide for temporary shortage of cash to maintain Cash Reserve Ratio and/or to meet unforeseen demand for funds.

(c) Alternative definition: In other words, call money is a method by which banks borrow from each other to be able to maintain the cash reserve ratio.

(d) Borrowers: Usually the banks who have temporary shortage of cash because of reserve requirements or unforeseen demand for funds, are the borrowers.

(e) Lenders: Usually the banks who have temporary excess of cash, are the lenders. But other financial institutions such as insurance companies, mutual funds and finance companies also operate in the call money market as suppliers of short term credit.

(f) Period: Call money is provided for very short period usually ranging from 1 day to 15, days.

(g) Over Telephone Market: The call money market is basically an over the telephone market.

(h) Alternative Name: It is called inter-bank call money market because usually the borrowers are the banks having shortage of cash and the lenders are also the banks having excess of cash.

Call Rate:

(i) The interest rate paid on call money loans is known as the call rate.

(ii) It is a highly volatile rate that varies from day to day sometimes even from hour to hour.

(iii) There is an inverse relationship between call rates and other short term money market instruments such as certificates of deposit and commercial paper.

(iv) A rise in call money rates makes other sources of finance (such as commercial paper and certificates of deposit) cheaper.

(iv) Certificate of deposit:

(a) Meaning: Certificates of Deposit (CD) are unsecured, negotiable, and short-term instruments in bearer form, issued by commercial banks and development financial institutions.

(b) To Whom Issued: These can be issued to individuals, corporations and companies during periods of tight liquidity when the deposit growth of banks is slow but the demand for credit is high.

(c) Period: They are issued for a period of 91 days to I Year:

(d) Purpose: These are issued to mobilize a large amount of money for short periods.

(v) Commercial Bill:

(a) Meaning: A commercial bill is a bill of exchange used to finance the working capital requirements of business firms. It is a short-term negotiable, self-liquidating instrument which is used to finance the credit sales of the firms.

(b) In other words:

(i) It is a written acknowledgement of debt, where seller (drawer) draws a bill of exchange and the buyer (drawee) accepts it. On being accepted, the bill becomes a marketable instrument and is called a Trade Bill.

(ii) Trade bills are commonly used in credit sales and purchase. A trade bill can be discounted with the bank if the seller (drawer) needs funds before the date of maturity of the bill. If the trade bill is accepted by a commercial bank, then it is known as Commercial Bill. The difference between the face value of the bill and the amount paid prior to the maturity date is called the discount charged by the bank.

(c) Period: These are generally issued for a period of 90 days.

(d) Negotiability: These are negotiable instruments i.e. they are freely transferable by endorsement and delivery.

Capital Market

(i) The term capital market refers to facilities and institutional arrangements through which long-term funds, both debt and equity are raised and invested.

(ii) Capital market satisfies long term financial needs of the government and industrial sector.

(iii) Capital market deals in medium and long - term securities i.e. equity shares and debentures.

(iv) Capital market is ideal when:

(a) Finance is available at reasonable cost.

(b) Financial institutions are sufficiently developed.

(c) Market operations are fair, competitive and transparent.

(d) Sufficient information is provided to the investors.

(e) Transaction cost are minimised.

(f) Capital is most productively allocated.

Distinction between Capital Market and Money Market

|

Capital Market |

Basis |

Money Market |

|

Financial institutions, Banks, corporate entities, foreign investors and retail investors. |

Participants |

Institutional participants such as RBI, commercial banks, financial institutions and finance company Individual investors normally do not participate. |

|

The main instruments traded are equity shares, debentures, bonds or preference shares, etc. |

Instruments |

The main instruments traded in the money market are short term debt instruments such as T-bills, trade bills reports, commercial paper and certificates of deposit. |

|

Securities do not necessarily require huge financial outlay. The value of units of securities is generally low i.e. ` 10, ` 100 and so is the case with minimum trading lot of shares which is kept small i.e. 5, 50, 100 or so. |

Investment outlay |

Transactions entail huge sums of money as the instruments are quite expensive.

|

|

Capital market deals in medium and long - term securities i.e. equity shares and debentures. |

Duration |

They have a maximum tenure of one year and may even be issued for single day. |

|

Capital Market Securities are considered more liquid investment because they are marketable on the stock exchanges. |

Liquidity |

Money market instruments on the other hand, enjoy a higher degree of liquidity as there is formal arrangement for this. The arrangement for this. The discount finance house of India (DFHI) has been established for a specific objective of providing a ready market for money market instruments. |

|

Capital market instruments are more riskier both with respect to returns and principal repayment. |

Safety |

Money market is generally much safer with a minimum risk of default. This is due to the shorter duration of investing and also to financial soundness of issues, which primarily are the government, banks and highly rated companies. |

|

The investment in capital markets generally yields a higher return for investors. |

Expected Return |

The expected return is less due to short duration. |

COMPONENTS OF CAPITAL MARKET

The Capital market can be divided into two parts:

(a) Primary Market (b) Secondary Market.

Primary Market (New Issue Market)

(i) Primary market is also known as the new issue market.

(ii) It deals with the new securities being issued for the first time.

(iii) The investors in this market are banks, financial institutions, insurance companies, mutual funds and individuals.

(iv) The essential function of a primary market is that it directly promotes capital formation because the flow of funds is directly from savers to entrepreneurs who utilize these funds for setting up new projects, expansion, diversification, modernization of existing projects, mergers and takeovers etc.

Methods of Floatation: There are various methods of floating new issues in the primary market:

1. Offer through prospectus:

(i) This involves inviting subscription from the public through issue of prospectus.

(ii) A prospectus makes a direct appeal to investors to raise capital, through an advertisement in newspaper and magazines.

(iii) Public issue involves a large number of intermediaries, such as bankers, brokers and underwriters.

(iv) This issue must be underwritten and listed at least on one stock market.

2. Offer for sale:

(i) Under this method securities are not issued directly to the public but are offered for sale through intermediaries like issuing houses or stock brokers.

(ii) In this case, a company sells securities enbloc at an agreed price to brokers who, in turn, resell them to the investing public.

3. Private placement:

(i) Private placement is the allotment of securities by a company to institutional investors (like LIC, UTI etc.) and some selected individuals.

(ii) It helps to raise capital more quickly than a public issue.

(iii) The cost of raising finance through private placement of securities is lower than that through public issue of securities.

(iv) Small companies which cannot afford to raise resources from the public issue, may opt for the private placement.

(v) It helps in also saving many mandatory and non-mandatory expenses.

4. Right issue:

(i) This is a privilege given to existing shareholders to subscribe to a new issue of shares according to the terms and conditions of the company.

(ii) The shareholders are offered the 'right' to buy new shares in proportion to the number of shares they already possess.

5. E-IPOs:

(i) A company proposing to issue capital to the public through the on-line system of the stock exchange has to enter into an agreement with the stock exchange. This is called an Initial Public Offer (IPO).

(ii) SEBI registered brokers have to be appointed for the purpose of accepting applications and placing orders with the company.

(iii) The issuer company should also appoint a registrar to the issue having electronic connectivity with the exchange.

Secondary Market

(i) The secondary market is also known as the stock market or stock exchange. It is a market for the purchase and sale of existing securities.

(ii) It helps existing investors to disinvest and fresh investors to enter the market.

(iii) It also provides liquidity and marketability to existing securities.

(iv) It also contributes to economic growth by channelizing funds towards the most productive investments through the process of disinvestment and reinvestment.

Stock Exchanges

(i) A stock exchange is an institution which provides a platform for buying and selling of existing securities.

(ii) According to Securities Contracts (Regulation) Act 1956, stock exchange means anybody of individuals, whether incorporated or not, constituted for the purpose of assisting, regulating or controlling the business of buying and selling or dealing in securities.

(iii) Ownership of existing securities is exchanged between investors.

(iv) Stock exchange are accessible from anywhere in the country through trading terminals.

The Functions of a Stock Exchange

(i) Providing liquidity and market ability to existing securities:

(a) Stock exchange provides a central market where securities can be bought and sold.

(b) Stock exchange gives investors the chance to disinvest and reinvest.

(c) This provides both liquidity and easy marketability to already existing securities in the market.

(ii) Pricing of securities:

(a) Prices of securities are determined by the forces of demand and supply for the securities.

(b) A stock exchange is a mechanism of constant valuation through which the prices of securities are determined.

(iii) Safety of transactions:

(a) In stock market only the listed securities are traded and stock exchange authorities include the companies names in the trade list only after verification of soundness of company.

(b) For listing, companies has to operate within the strict rules and regulations. Even after listing, the company has to operate within the legal framework of stock exchange. This ensures safety of dealing through stock exchange.

(iv) Contribution to economic growth:

(a) A stock exchange is a market in which existing securities are resold or traded.

(b) Through this process of disinvestment and reinvestment savings get channelized into their most productive investment avenues. This leads to capital formation and economic growth.

(v) Spreading of equity cult: The stock exchange can play a vital role in ensuring wider share ownership by regulating new issues, better trading practices and taking effective steps in educating the public about investments.

(vi) Providing scope for speculation:

(a) In stock exchange market, speculators can generate profits from the fluctuations in security prices.

(b) The stock exchange provides scope of speculation in a restricted and controlled manner.

(c) A certain degree of healthy speculation is necessary to ensure liquidity and price continuity in the stock market.

Distinction between Primary Market and Secondary Market

|

Primary Market (New Issue Market) |

Basis |

Secondary Market (Stock Exchange) |

|

There is sale of securities by new companies or further (new issues of securities by existing companies to |

Nature of securities |

There is trading of existing shares only. |

|

Securities are sold by the company to the investor directly (or through an intermediary. |

Process of Transactions |

Ownership of existing securities is exchanged between investors. The company is not involved at all. |

|

The flow of funds is from savers to investors, i.e. the primary market directly promotes capital formation. |

Capital Formation |

Enhances encashability (liquidity) of shares, i.e. the secondary market indirectly promotes capital formation. |

|

Only buying of securities takes place in the primary market, securities cannot be sold there. |

Buying or selling |

Both the buying and the selling of securities can take place on the stock exchange. |

|

Prices are determined and decided by the management of the company. |

Determination of Prices |

Prices are determined by demand and supply for the security. |

|

There is no fixed geographical location. |

Location |

Located at specified places. |

TRADING AND SETTLEMENT PROCEDURE

(i) Trading in securities is now executed through an on - line, screen - based electronic trading system, simply put, all buying and selling of shares and debentures are done through a computer terminal.

(ii) There was a time when in the open outcry system, securities were bought and sold on the floor of the stock exchange. Under this auction system, deals were struck among brokers, prices were shouted out and the shares sold to the highest bidder.

(iii) However, now almost all exchanges have gone electronic and trading is done in the broker's office through a computer terminal.

(iv) A stock exchange has its main computer system with many terminals spread across the country. Trading in securities is done through brokers who are members of the stock exchange. Trading has shifted from the stock market floor to the broker's office.

(v) Every broker has to have access to a computer terminal that is connected to the main stock exchange. In the screen - based trading, a member logs on to the site and any information about the shares (company, member, etc.) he wishes to buy or sell and the price is fed into the computer.

(vi) The computer in the broker's office is constantly matching the orders at the best bid and offer price.

(vii) Those that are not matched remain on the during the day i.e., between 9.15 am to 3.30 pm (From Monday to Friday).

ADVANTAGES OF ELECTRONIC TRADING SYSTEM OR SCREEN-BASED TRADING

1. Ensures Transparency:

(a) It ensures transparency as it allows participants to see the prices of all securities in the market while business is being transacted.

(b) They are able to see the full market during real time.

2. Increases efficiency:

(a) It increases efficiency of information being passed on, thus helping in fixing prices efficiently.

(b) The computer screens display information on prices and also capital market developments that influence share prices.

3. Increases efficiency of operation: It increases the efficiency of operation, since there is reduction in time, cost and risk of error.

4. Improving the liquidity of the market:

(a) It improves liquidity of the stock market as people from all over the country and even from abroad participate in the stock market and can buy or sell securities through brokers or members without knowing each other,

(b) It means they can sit in the broker's office, log on to the computer at the same time and buy or sell securities.

5. Provides Single Trading Platform:

(a) A single trading platform has been provided as business is transacted at the same time in all the trading centres.

(b) Thus, all the trading centres spread all over the country have been brought onto one trading platform, i.e., the stock exchange, on the computer.

DEMATERIALISATION (DEMAT ACCOUNT) AND DEPOSITORIES

(i) The process of holding securities in an electronic from is called dematerialization (D'mat Account).

(ii) All trading in securities is now done through computer terminals. Since all systems are computerized, buying and selling of securities are settled through an electronic book entry form.

(iii) This is mainly done to eliminate problems like theft, fake / forged transfers, transfer delays and paper work associated with share certificates or debentures held in physical form.

(iv) This is a process where securities held by the investor in the physical form are cancelled and the investor is given an electronic entry or number so that she / he can hold it as an electronic balance in an account. This process of holding securities in an electronic from is called dematerialization.

(v) For this, the investor has to open a demat account with an organization called a depository.

(vi) In fact, Now all Initial Public Officer (IPOs) are issued in dematerialization form and more than 99% of the turnover is settled by delivery in the demat form.

(vii) The Securities and Exchange Board of India (SEBI) has made it mandatory for the settlement procedure to take place in demat form in certain select securities.

(viii) Holding shares in demat form is very convenient as it is just like a bank account. Physical shares can be converted into electronic form (dematerialisation) or electronic holdings can be reconverted into physical certificates (rematerialisation).

(ix) Dematerialisation enables shares to be transferred to some other account just like cash and ensure settlement of all trades through a single account in shares.

Working of a Demat System

1. A depository participant (DP), either a bank, broker, or financial services company, may be identified.

2. An account opening form and documentation (PAN card details, photograph, and power of attorney) may be completed.

3. The physical certificate is to be given to the DP along with a dematerialization request form.

4. If shares are applied in a public offer, simple details of DP and demat account are to be given and the shares on allotment would automatically be credited to the demat account.

5. If shares are to be sold through a broker, the DP is to be instructed to debit the account with the number of shares.

6. The broker then gives instruction to his DP for delivery of the shares to the stock exchange.

7. The broker then receives payment and pay the person for the shares sold.

8. All these transactions are to be completed within 2 days, i.e., delivery of shares and payment received from the buyer is on a T + 2 basis, settlement period.

Depository

(i) Depository is an organisation which holds securities (like shares, debentures, bonds, etc.) of investors in electronic form at the request of the investors through a registered depository Participant.

(ii) Just like a bank keeps money in safe custody for customers, a depository also is like a bank and keeps securities in electronic form on behalf of the investor.

(iii) In the depository a securities account can be opened, all shares can be deposited, they can be withdrawn/ sold at any time and instruction to deliver or receive shares on behalf of the investor can be given.

(iv) It is a technology driven electronic storage system. It has no paper work relating to share certificates, transfer, forms, etc. All transactions of the investors are settled with greater speed, efficiency and use as all securities are entered in a book entry mode.

(v) In India, there are two depositories.

(a) National Securities Depositories Limited (NSDL): It is the first and largest depository presently operational in India. It was promoted as a joint venture of the IDBI, UTI, and the National Stock Exchange.

(b) The Central Depository Services Limited (CDSL): It is the second depository to commence operations and was promoted by the Bombay Stock Exchange and the Bank of India.

STEPS IN THE TRADING AND SETTLEMENT PROCEDURE

It has been made compulsory to settle all trades within 2 days of the trade date, i.e., on a T + 2 basis, since 2003.

The following steps are involved in the screen - based trading for buying and selling of securities:

1. Selection of Broker:

(i) If an investor wishes to buy or sell any security he has to first approach a registered broker or sub-broker and enter into an agreement with him.

(ii) The investor has to sign a broker-client agreement and a client registration form before placing an order to buy or sell securities. He has also to provide certain other details and information. These include:

· PAN number (This is mandatory).

· Date of birth and address.

· Educational qualification and occupation.

· Residential status (Indian/NRI).

· Bank account details.

· Depository account details.

· Name of any other broker with whom registered.

· Client code number in the client registration form.

· The broker then opens a trading account in the name of the investor.

The broker then opens a trading account in the name of the investor.

2. Opening Demat account: The investor has to open a 'demat' account of 'beneficial owner' (BO) account with a depository participant (DP) for holding and transferring securities market.

3. Placing the Order:

(i) The investor then places an order with the broker to buy or sell shares.

(ii) Clear instructions have to be given about the number of shares and the price at which the shares should be bought or sold.

(iii) The broker will then go ahead with the deal at the above mentioned price or the best price available. An order confirmation slip is issued to the investor by the broker.

4. Executing the order:

(i) The broker then will go on - line and connect to the main stock exchange and match the share and best price available.

(ii) When the shares can be bought or sold at the price mentioned, it will be communicated to the broker's terminal and the order will be executed electronically. The broker will issue a trade confirmation slip to the investor.

(iii) After the trade has been executed, within 24 hours the broker issues a Contract Note. This note contains details of the number of shares bought or sold, the price, the date, and time of deals, and the brokerage charges. This is an important document as it is legally enforceable and helps to settle disputes/ claims between the investor and the broker.

(iv) A Unique Order Code number is assigned to each transaction by the stock exchange and is printed on the contract note.

5. Settlement

(i) Now, the investor has to deliver the shares sold or pay cash for the shares bought. This should be done immediately after receiving the contract note or before the day when the broker shall make payment or delivery of shares to the exchanges. This is called the pay - in day.

(ii) Cash is paid or securities are delivered on pay -in day, which is before the T + 2 day as the deal has to be settled and finalized on the T + 2 day. The settlement cycle is on T + 2 day on a rolling settlement basis, w.e.f. 1 April 2003.

(iii) On the T + 2 day, the exchange will deliver the share or make payment to the other broker. This is called the pay - out day. The broker then has to make payment to the investor within 24 hours of the payout day since he has already received payment from the exchange.

(iv) The broker can make delivery of shares in demat form directly to the investor's demat account. The investor has to give details of his demat account and instruct his depository participant to take delivery of securities directly in his +beneficial owner account.

SECURITIES AND EXCHANGE BOARD OF INDIA (SEBI)

(i) Securities and Exchange Board of India SEBI is the regulatory body for the investment market in India. The purpose of this board is to maintain stable and efficient markets by creating and enforcing regulations in the marketplace.

(ii) The Securities and Exchange Board of India was established by the Government of India on 12 April, 1988 as an interim administrative body to promote orderly and healthy growth of securities market and for investor protection.

Objectives of SEBI

(i) To regulate stock exchanges to promote their orderly functioning.

(ii) To protect the rights and interests of investors to guide and educate them.

(iii) To prevent trading malpractices and to achieve a balance between self-regulation by the securities industry and its statutory regulation.

(iv) To regulate and develop a code of conduct and fair practices by intermediaries like brokers, merchant bankers etc.

Functions of SEBI

The functions of SEBI are:

1. Regulatory functions of SEBI:

(i) Registration of brokers and sub-brokers other players in the market.

(ii) Registration of collective investment schemes and Mutual funds.

(iii) Regulation of stock brokers, portfolio exchanges underwriters and merchant brokers and any other securities Market.

(iv) Calling for information by undertaking inspection, conducting enquires and audits of stock exchanges and intermediaries.

(v) Regulation of takeover bids by companies.

(vi) Levying fee or other charges for carrying out the purposes of the Act.

(vii) Performing and exercising such power under Securities Contracts (regulation) Act 1956, as may be delegated by the Government of India.

2. Development functions:

(i) Training of intermediaries of the securities market.

(ii) Conducting research and publishing information useful to all market participants.

(iii) Undertaking measures to develop the capital markets by adapting a flexible approach.

3. Protective functions:

(i) Prohibition of fraudulent and unfair trade practices like making misleading statements, manipulations, price rigging, etc.

(ii) Controlling insider trading and imposing penalties for such practices.

(iii) Undertaking steps for investor protection.

(iv) Promotions of fair practices and code of conduct in securities market.

Note: 1. Price Rigging:

(i) The act of businesses conspiring together to artificially inflate or depress the market price of securities.

(ii) Price rigging is an illegal practice and is SEBI aims to prohibit as they can cheat investors.

2. Insider Trading:

(i) Buying and selling of securities of a public traded firm by an insider to benefit from insider information of the company.

(ii) Insider trading is restricted or prohibited by SEBI.

Words that Matter

1. Financial market: It refers to a market which as a link of an intermediary between savers and investors by mobilising funds between them.

2. Financial intermediation: The process by which allocation of funds is done is called financial intermediation.

3. Money market: Money market is a market for short-term funds which deals in monetary assets whose period of maturity is up to one year.

4. Treasury bills: Treasury bills (or T-bills) is an instrument (in the form of promissory note) of short-term borrowing by the government which is issued by the Reserve Bank of India on behalf of the Government of India at discount for maturing in less than one year.

5. Commercial paper: Commercial paper is a short-term unsecured promissory note, negotiable and transferable by endorsement and delivery with a fixed maturity period.

6. Call money: Call money is a short-term finance repayable on demand, with a maturity period of one day to fifteen days, used for inter-bank transactions.

7. Certificate of deposit: Certificate of Deposit (CD) are unsecured, negotiable, short- term instruments in bearer form, issued by commercial banks and development financial institutions.

8. Commercial bill: Commercial bill is a bill of exchange used to finance the working capital requirements of business firms. It is a short-term negotiable, self-liquidating instrument which is used to finance the credit sales of the firms.

9. Capital market: The term 'capital market' refers to facilities and institutional arrangements through which long-term funds, both debt and equity are raised and invested.

10. Primary market: Primary market is also known as the new issue market. It deals with the new securities being issued for the first time. The investors in this market are banks, financial institutions, insurance companies, mutual funds and individuals.

11. Secondary market: The secondary market is also known as the stock market or stock exchange. It is a market for the purchase and sale of existing securities.

12. Stock exchange: Stock exchange is an institution which provides a platform for buying and selling of existing securities.

13. Dematerialization: The process of holding securities in an electronic form is called dematerialization (D'mat Account).

14. Depository: Depository is an organisation which holds securities (like shares, debentures, bonds, etc.) of investors in electronic form at the request of the investors through a registered depository participant.

15. Securities and Exchange Board of IndiaSEBI: It is a regulatory body for the investment market in India. The purpose of this board is to maintain stable and efficient markets by creating and enforcing regulations in the marketplace.

You need to login to perform this action.

You will be redirected in

3 sec